GN 2.3: Sustainability reporting initiatives

Guidance Note purpose

The purpose of this Guidance Note is to provide asset managers, property managers and facilities managers with a broad understanding of some of the key related sustainability reporting initiatives undertaken by asset managers that require data and documentation to be provided

Context

Alongside an annual E.S.G. report, or the sustainability section of an annual financial report, there are a variety of mandatory and voluntary sustainability reporting initiatives that run throughout the year. Some of these schemes are set at the performance of an individual property, whereas others are focused at a fund or client level.

Most of these reporting initiatives will require specific data and documentation to be gathered and collated, either directly by the asset manager, or though co-ordination by a property or facilities manager.

While voluntary schemes are assessed against the same criteria wherever they are adopted, there are differences between how statutory schemes are applied in each of the devolved administrations. For example, Energy Performance Certificates involve a different assessment methodology and set of compliance obligations in Scotland compared to the rest of the UK.

Importance

There are a number of reasons why companies participate in sustainability reporting initiatives. For example:

- They may be legally required to do participate.

- Stakeholders demand their participation.

- Participation may be a means of measuring success against their own corporate strategy.

Participating in sustainability reporting initiatives can:

- Enable sustainability performance of a property, portfolio of asset manager to be promoted to a range of stakeholders.

- Support engagement with investors, some of which may require public disclosure f sustainability information before committing to investment.

- Contribute towards meeting occupiers’ requirements, where participation in a sustainability reporting initiat8ive may demonstrate alignment with broader sustainability objectives.

- Provide valuable feedback in terms of benchmarking performance against peers, and identifying opportunities for continual improvement.

Responsibilities & Interests

The table below lists a rage of key sustainability reporting initiatives. This list is not exhaustive, and will evolve to account for new legislation, and new or evolving voluntary schemes. Asset managers, property managers and facilities managers are likely to have a responsibility or specific interest across all schemes.

- AM - Asset Manager

- PM - Property Manager

- FM - Facilities Manager

1. Mandatory Greenhouse Gas Reporting

Stakeholder:

2. Streamlined Energy and Carbon Reporting

Stakeholder:

3. Global Real Estate Sustainable Benchmark

Stakeholder:

4. Carbon Disclosure Project

Stakeholder:

5. European Association for Investors in Non-Listed Real Estate Vehicles

Stakeholder:

6. European Public Real Estate Sustainable Best Practices Recommendations

Stakeholder:

7. Global Reporting Initiative Construction and Real-Estate Sector Supplement

Stakeholder:

8. Real Estate Environmental Benchmark

Stakeholder:

How to

Intro

A Property manager should have a clear understanding of the requirements of each reporting scheme and what they represent as well as being able to facilitate activities that improve performance.

Usually, the decision to participate in a sustainability reporting initiative instructed by the asset manager and the process of installing and managing advanced meters is coordinated by the property manager with input from the facilities manager.

1: Mandatory Greenhouse Gas Reporting

Mandatory Greenhouse Gas Reporting (MGHR) (known as GHG reporting) was introduced in 2013 to allow investors to incorporate emissions, energy and other resource efficiencies into their analyses and provide greater disclosure on quotable organisations environmental performance.

MGHR requires that all UK quoted companies report on their greenhouse gas emissions in the Directors report section of the company annual report. GHG reporting affects all UK incorporated companies listed on the main market of:

- The London Stock Exchange (FTSE).

- European Economic Area Market.

- New York Stock Exchange (NYSE).

- American/Canadian Stock Exchange (NASDAQ).

The yearly reporting of GHG emissions requires an organisation to have accountable data management systems for energy use and other sources of emissions across its property portfolio.

It is important that energy use data is reliably tracked because:

- It helps to judge performance of individual properties and to assess where to take action.

- The GHG emissions will be reported within the companies’ annual reports and accounts and will therefore be very visible to investors and other stakeholders.

The use of an intensity ratio, such as per unit of turnover, should allow comparison of a company’s performance. The reporting is expected to drive investment in energy efficiency.

Property managers will have a requirement to support asset managers and occupiers in relation to their GHG emission reporting requirements. This may involve collecting and recoding relevant data for the properties they manage on their behalf.

2: Streamlined Energy and Carbon Reporting

The Companies (Directors’ Report) and Limited Liability Partnerships (Energy and Carbon Report) Regulations 2018 implement the government’s policy on Streamlined Energy and Carbon Reporting (SECR).

SECR was introduced as the Carbon Reduction Commitment (CRC) Energy Efficiency Scheme came to an end. The Regulations build on existing obligations, such as mandatory greenhouse gas (GHG) reporting and the Energy Saving Opportunity Scheme (ESOS), for example.

Organisations in scope of SECR should report all energy use and associated GHG emissions that they are responsible for.

In the case of asset manager-occupier arrangements, the party responsible for the consumption of energy should take the responsibility for reporting of it under this legislation. This should include:

- consumption of energy in rented serviced areaswhere a tenant would report on energy consumption.

- despite not being directly responsible for its purchase.

- if information on energy consumption is available through sub-meters,for example.

- or provide estimates where information is not available..

In turn, asset managers should report on energy purchased for areas of a property they are obligated to manage either directly or via a Property Manager.

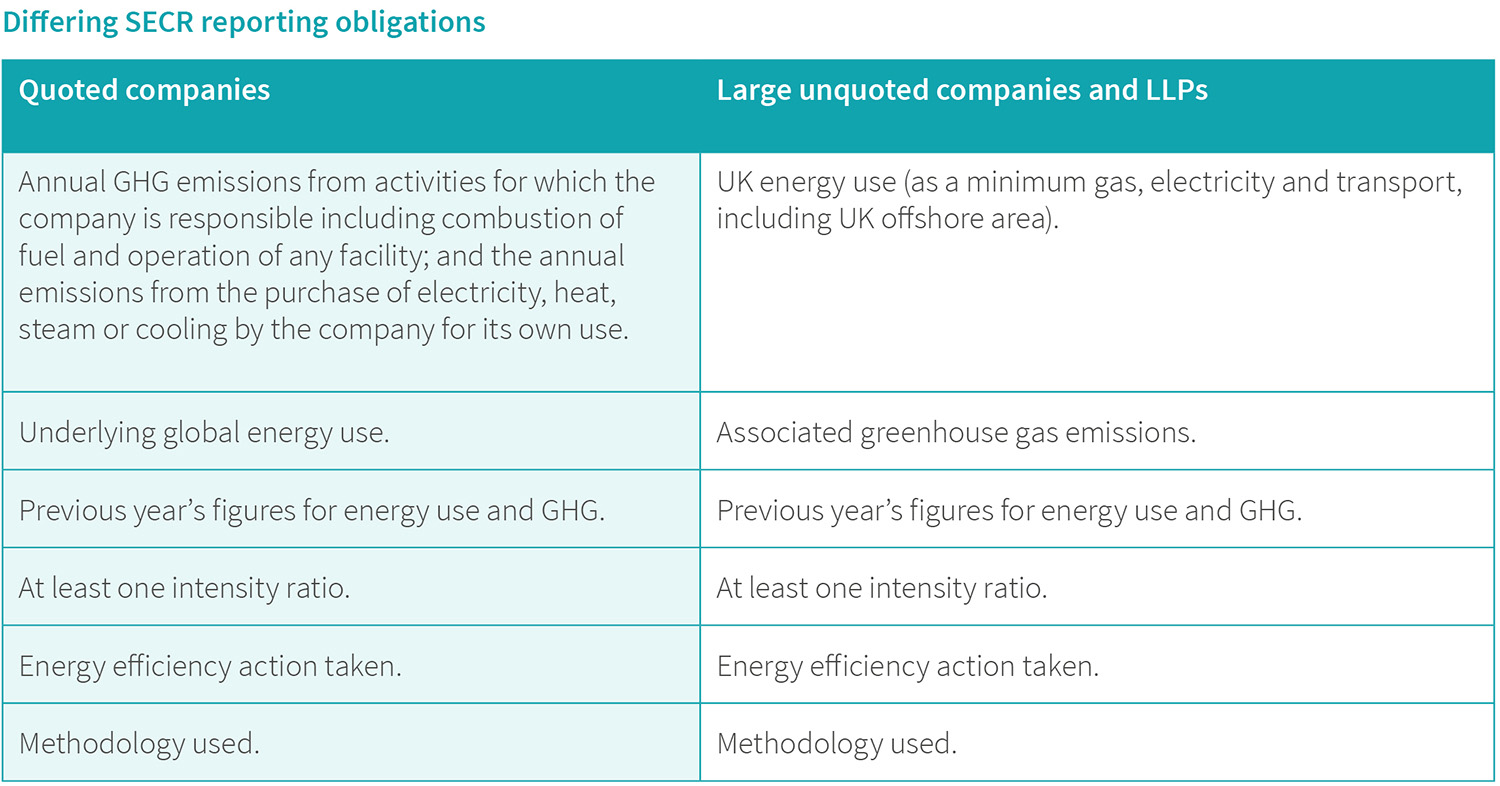

SECR extends the reporting requirements for quoted companies and mandates new annual disclosures for large unquoted and limited liability partnerships (LLPs).

The reporting obligations differ between quoted companies and unquoted companies or LLPs summarized are summarized in the table below:

3: Global Real Estate Sustainable Benchmark

Global Real Estate Sustainable Benchmark (GRESB) is an international membership organisation for institutional real estate investors and investment managers. GRESB provides a benchmarking framework for listed and non-listed companies to annually assess the sustainability performance of their property portfolios.

An increasing number of investors are requiring property companies and fund managers to take part in GRESB to demonstrate their sustainability performance.

The GRESB Survey captures almost 50 data points measuring sustainability, including environmental and social factors. The data collected includes environmental performance indicators, such as energy consumption, GHG emissions, water consumption and waste, as well as management processes and practices, such as policies, risk assessments and social indicators, for example, occupier engagement.

The survey is undertaken on an annual basis and all buildings which have been part of the portfolio at some point that year must be reported on.

4: Carbon Disclosure Project

The Carbon Disclosure Project (CDP) is a voluntary global carbon reporting system through which thousands of organisations, including such as banks, pension funds, asset managers, insurance companies and foundations, report their climate, water and forest related risks and performance.

There are specific programmes for which data can be supplied including:

- Investor CDP: A request for companies’ greenhouse gas emissions, water usage and strategies for managing climate change and water risks.

- CDP Supply Chain: An annual process that results in consistent information from suppliers on climate and water-related strategy and action.

- CDP Water Program: A questionnaire for the world's largest companies from water-intensive industry sectors or those which may be exposed to water-related risks in their supply chain.

- CDP Cities: Voluntary climate change reporting framework open to any city government, regardless of their size or location.

As participation in the CDP involves considerable data gathering activities, having established data management arrangements is advantageous.

5: European Association for Investors in Non-Listed Real Estate Vehicles

The European Association for Investors in Non-Listed Real Estate Vehicles (INREV) have developed a set of specific reporting guidelines aimed at encouraging meaningful dialogue on sustainability between investors and fund managers.

The guidelines are designed to enable the provision of a structured and clear report that:

- Outlines the ESG Strategy at the manager and vehicle level.

- Explain the annual objectives, translated from the strategy, and how they are implemented.

- Provide concrete action plans at the asset level accompanied by an annual report on progress of these plans.

- Report against specific environmental key performance indicators.

Property Managers may be responsible for preparing and maintaining, or contributing to, the production of asset sustainability plans, reporting key environmental data in line with the INREV guidelines, and evidencing the appropriate management of legislative and environmental risks.

6: European Public Real Estate Sustainable Best Practices Recommendations

The European Public Real Estate (EPRA) Sustainable Best Practices Recommendations (sBPR) covers companies’ investment activities, its own occupied property, and corporate-level policies and practices. sBPR excludes real estate development activities.

Data must be provided against a range of sustainability performance measures with those relating to investment activities fall under one of two broad categories:

- Environmental Sustainability Performance Measures (covering utilities, waste, and certification).

- Social Performance Measures (covering H&S, community engagement, and social impact assessment).

7: Global Reporting Initiative Construction and Real-Estate Sector Supplement

The Global Reporting Initiative (GRI) has pioneered and developed a comprehensive Sustainability Reporting Framework that is widely used around the world. The GRI framework enables organisations to measure and report their economic, environmental, social and governance performance in a consistent manner.

It is the most internationally recognised sustainability reporting standard, and many property sector companies choose to report in line with it. GRI has produced a Construction and Real-Estate Sector Supplement (CRESS) which contains guidance on reporting specific to this sector.

CRESS covers a wide range of issues and property managers will need to be aware of common environmental performance indicators used for sustainability reporting and include:

- Energy: Organisational direct and indirect energy use, for example, the amount of energy produced on-site through the burning of gas in kWh’s.

- Water: Water withdrawal or percentage and total volume of water recycled or reused, for example, metered utility data or rainwater collected directly and stored on site.

- Biodiversity: Potential impact on land that contains or is adjacent to legally protected areas or areas of high biodiversity value, for example, biological survey results of protected species or habitats found in amenity spaces.

- Emissions, effluents and waste: Direct and indirect greenhouse gas emissions, ozone depleting substances by type and weight and the total weight of waste by type and disposal method, for example, total weight in tonnes of hazardous waste disposed of in landfill.

The CRESS reporting measures are based around an organisation’s level of control or influence over its impacts, and as a result, reporting boundaries will vary for each organisation, and also depending on how their building is occupied and managed, for example, multi-let, single let etc.

8: Real Estate Environmental Benchmark

The Real Estate Environmental Benchmark (REEB) is a publicly available benchmark based on operational environmental performance for commercial properties in the UK.

REEB is one of the only benchmarks based on the performance of buildings ‘in-use’ and is increasingly becoming the industry standard used by investors, fund managers and property owners to compare the performance of commercial properties across the UK.

The benchmark currently assesses performance against energy and water across a ranges of asset types:

- Office (Non-Air Conditioned).

- Office (Air Conditioned).

- Enclosed Shopping Centre (Non-Air Conditioned).

- Enclosed Shopping Centre (Air Conditioned).

- Unenclosed Shopping Centre/Shopping Village.

- Retail, Leisure and Industrial Park.

- Car Park (Multi Storey).

- Car Park (Open Air).

Property managers must make the required data available for submission to the Better Building Partnership on at least an annual basis for electricity, gas, and water along with up-to-date building characteristics to ensure the intensity metrics developed via the benchmarking process are accurate.

Through the Managing Agents Partnership there has been agreement to expand the data collection beyond Better Building Partnership member portfolios, with an aim at improving the accuracy of the benchmark as a reflection of operational asset performance. Waste data will also be reviewed following the development of the Standardised Waste Reporting Framework aimed at improving this dataset.

Related Guidance Notes

The following Guidance Notes contain related information:

- GN1.4: The wider risk context

- GN2.2: Automating property level data

- GN3.1: Rating and certifications

- GN4.5: Energy consumption profile

- GN4.7: Benchmarking energy use and setting targets

- GN5.3: Benchmarking water use and setting targets

- GN8.1: What is social value?

- GN9.1: Modern Slavery Act

- GN9.2: Living Wage Foundation certified services

- GN11.2: Engaging occupiers

- GN12.1: Biodiversity baseline

- GN12.2: Valuable green spaces

- GN13.3: Occupier satisfaction surveys

Additional resources

- BBP Real Estate Environmental Benchmark

- MAP Improving Waste Management Practices Standardised Reporting Framework

- UK Government: Environmental Reporting Guidelines

- UK Government: Mandatory Greenhous Gas Emissions

- UK Government: Streamlined Energy and Carbon Reporting

- The Global ESG Benchmark for Real Estate

- The Carbon Disclosure Project

- European Association for Investors in Non-Listed Real Estate Vehicles

- European Public Real Estate Sustainable Best Practices Recommendations

- Global Reporting Initiative Construction and Real-Estate Sector Supplement

Solutions Scrapbook

Module 2 - Practical Implementation

- Prioritising ESG interventions throughout the property investment lifecycle, including integration into asset business plans and the growing role of sustainable finance.

- Ways of engaging with other stakeholders, such as occupiers and operating partners, to secure the delivery of ESG interventions and outcomes.

- Establishing roles and responsibilities,ensuring accountability and incentivising action across the value chain.

- Market leadership: examples of best practice and innovation from around the sector.